Remember to permit JavaScript if it is disabled in your browser or obtain the details by the backlinks provided down below.

February 12, 2021

Federal Reserve Board releases hypothetical scenarios for its 2021 bank worry assessments

For release at nine:15 a.m. EST

The Federal Reserve Board on Friday launched the hypothetical scenarios for its 2021 bank worry assessments. Previous year, the Board discovered that significant financial institutions ended up frequently well capitalized less than a range of hypothetical gatherings but because of to continuing financial uncertainty put constraints on bank payouts to protect the strength of the banking sector.

The Board’s worry assessments aid make certain that significant financial institutions are in a position to lend to homes and corporations even in a serious recession. The exercise evaluates the resilience of significant financial institutions by estimating their bank loan losses and capital levels—which offer a cushion against losses—under hypothetical recession scenarios that prolong 9 quarters into the future.

“The banking sector has provided important support to the financial restoration about the past year. While uncertainty stays, this worry examination will give the public supplemental details on its resilience,” Vice Chair for Supervision Randal K. Quarles reported.

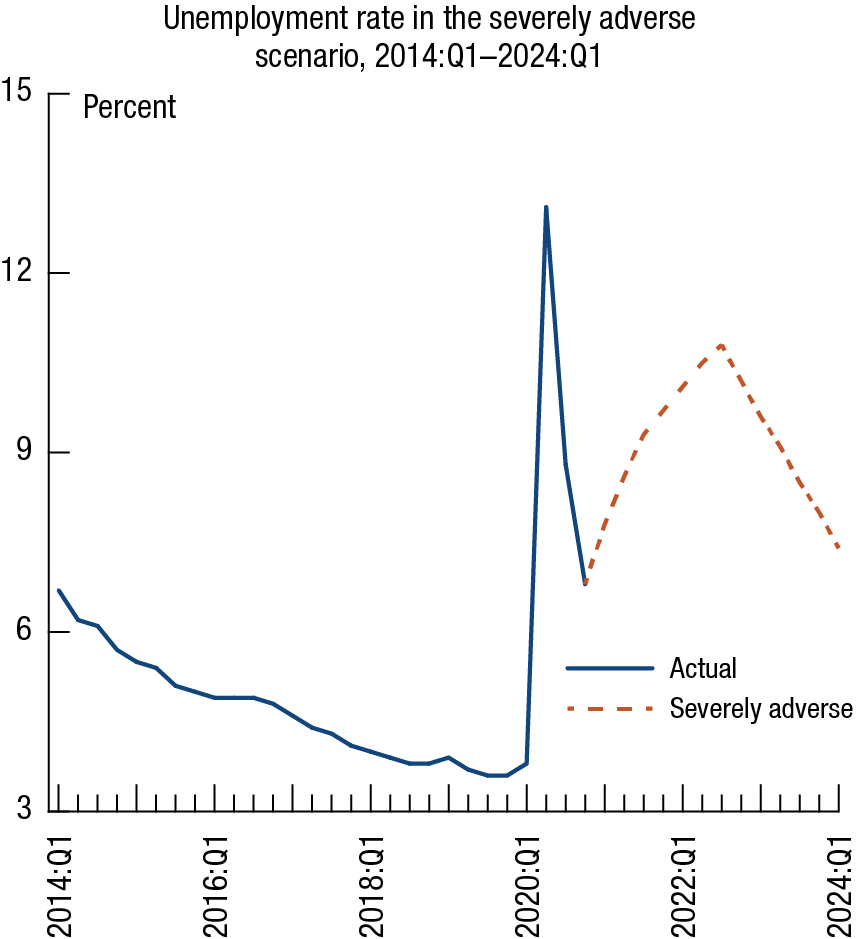

The hypothetical recession begins in the initially quarter of 2021 and features a serious world-wide downturn with significant worry in industrial genuine estate and company financial debt marketplaces. The U.S. unemployment charge in the “severely adverse” situation rises by four share points from its starting off level, achieving a peak of ten-three/four percent in the 3rd quarter of 2022. Gross domestic product falls four percent from the fourth quarter of 2020 by the 3rd quarter of 2022, with asset price ranges dropping sharply, including a 55 percent decline in equity price ranges. The chart down below exhibits the path of the unemployment charge:

This year, 19 significant financial institutions will be subject matter to the worry examination. Smaller financial institutions are on a two-year worry examination cycle but can decide in to this year’s examination and need to do so by April 5. Financial institutions with significant buying and selling operations will be examined against a world-wide market shock element that stresses their buying and selling, non-public equity, and other reasonable price positions. Additionally, financial institutions with significant buying and selling or processing operations will be examined against the default of their most significant counterparty. A desk down below exhibits the parts that would use to every bank, as well as identifying which financial institutions are on a two-year cycle, primarily based on knowledge as of September thirty, 2020.

The scenarios are not forecasts and the severely adverse situation is drastically more serious than most current baseline projections for the path of the U.S. financial state less than the worry tests period of time. They are made to assess the strength of significant financial institutions all through hypothetical recessions, which is specifically appropriate in a period of time of uncertainty. Every situation features 28 variables covering domestic and global financial action.

| Bank | Subject to 2021 worry examination | Can decide in to 2021 worry examination | Subject to world-wide market shock | Subject to counterparty default |

|---|---|---|---|---|

| Ally Monetary Inc. | X | |||

| American Convey Enterprise | X | |||

| Bank of America Company | X | X | X | |

| The Bank of New York Mellon Company | X | X | ||

| Barclays US LLC | X | X | X | |

| BMO Monetary Corp. | X | |||

| BNP Paribas Usa, Inc. | X | |||

| Funds One particular Monetary Company | X | |||

| Citigroup Inc. | X | X | X | |

| Citizens Monetary Group, Inc. | X | |||

| Credit Suisse Holdings (Usa), Inc. | X | X | X | |

| DB Usa Company | X | X | X | |

| Discover Monetary Products and services | X | |||

| Fifth Third Bancorp | X | |||

| The Goldman Sachs Group, Inc. | X | X | X | |

| HSBC North America Holdings Inc. | X | X | X | |

| Huntington Bancshares Incorporated | X | |||

| JPMorgan Chase & Co. | X | X | X | |

| KeyCorp | X | |||

| M&T Bank Company | X | |||

| Morgan Stanley | X | X | X | |

| MUFG Americas Holdings Company | X | |||

| Northern Rely on Company | X | |||

| The PNC Monetary Products and services Group, Inc. | X | |||

| RBC US Group Holdings LLC | X | |||

| Locations Monetary Company | X | |||

| Santander Holdings Usa, Inc. | X | |||

| Condition Road Company | X | X | ||

| TD Group US Holdings LLC | X | |||

| Truist Monetary Company | X | |||

| UBS Americas Keeping LLC | X | |||

| U.S. Bancorp | X | |||

| Wells Fargo & Enterprise | X | X | X |

Previous Update:

February 12, 2021

More Stories

Top 10 Marketing Concepts For Small Business Marketing

Why Sales and Marketing MUST Align

Affiliate Marketing Coach – Speed Up Your Affiliate Progress With A Coach